01

Tax Calendar

Track deadlines by client, entity, state, tax type, frequency, owner, and status.

Explore moduleManage client tax calendars, filings, registrations, notices, follow-ups, and confirmations in one simple workspace.

Existing AtomicTax client? Log in to upload reports, view filing status, and access confirmations.

AtomicTax turns deadline tracking, report requests, registrations, notices, and filing confirmations into a shared firm workspace.

AtomicTax gives accounting firms one place to manage the operational side of tax work: calendars, filings, registrations, notices, client follow-up, and confirmations.

Track deadlines by client, entity, state, tax type, frequency, owner, and status.

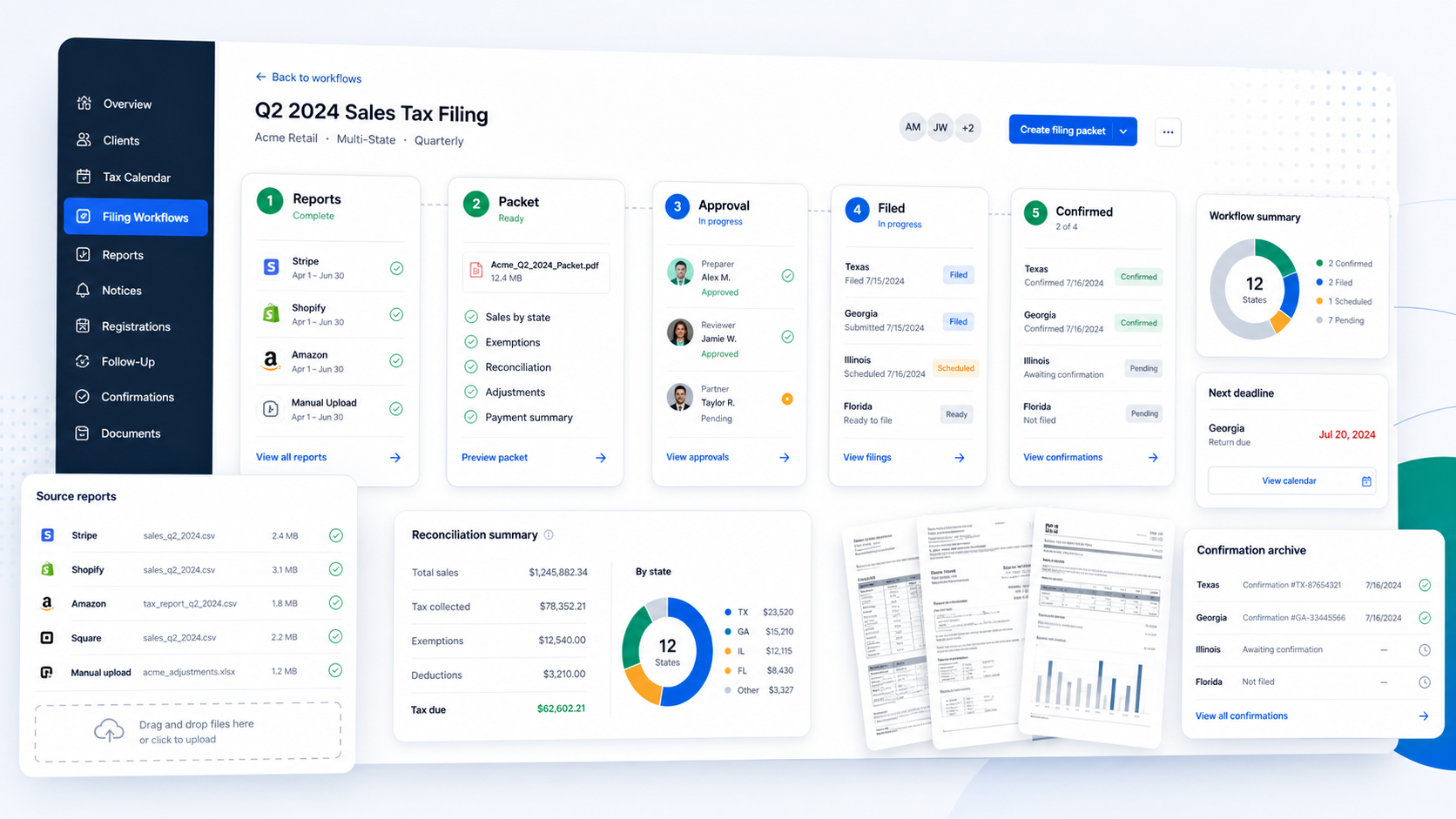

Explore moduleCollect reports, prepare filing packets, route approvals, file returns, and store confirmations.

Explore moduleUpload notices, assign owners, track response deadlines, and keep resolution history.

Explore moduleManage state registrations, permit details, account numbers, filing frequencies, and first-return deadlines.

Explore moduleAutomate reminders for missing reports, approvals, forms, and client answers.

Explore moduleKeep filed returns, confirmations, payment details, and packet history organized by client.

Client workspaceExisting AtomicTax clients can continue using the client workspace to upload reports, track filing status, review requests, and access filing confirmations.

Load reports for a client, build the packet, route approval, file the return, and archive the confirmation in one workflow.

The accountant platform remains primary, while direct business filing support stays easy to find for existing and new business clients.

Firm-wide tax operations across every client.

View pageDirect filing support for merchants and business owners.

View pageLogin, upload reports, review requests, and find confirmations.

View pageSimple filing and registration pricing, with firm demos for platform setups.

View page